The SECI

Views From the Marsh - David Owen

Once we have looked at the evidence I am sure we will writing about whether, if he were to become PM, Andy Burnham can replicate the stronger growth of Manchester on the national UK stage, but worth noting that today’s payroll data (which have a habit of leading the more widely quoted LFS figures) showed a further acceleration in median UK earnings (to 4.9% year-on-year, but more importantly 7.4% annualised in the three months ending April, the highest figure recorded since December 2024).

We may take issue with our good friend and former colleague Albert Edwards warning of the return of 10% inflation (see our recent post, “Time to make a major asset allocation switch?” here), but clearly inflationary pressures remain elevated, even before higher energy costs and food prices feed through. This alone would justify bond markets being on high alert.

Important to note, that real wage growth will help underpin some of the positive momentum still being seen in economic activity (with GDP up 0.6% in Q1, causing the IMF to nudge up its 2026 UK forecast from 0.8% to 1%). No one should want the economy to suddenly crack and a recession to follow.

However, for this short post, we thought it timely to remind readers of the SECI (the Saltmarsh Economics Climate Index), which ranks countries and sovereigns on climate grounds.

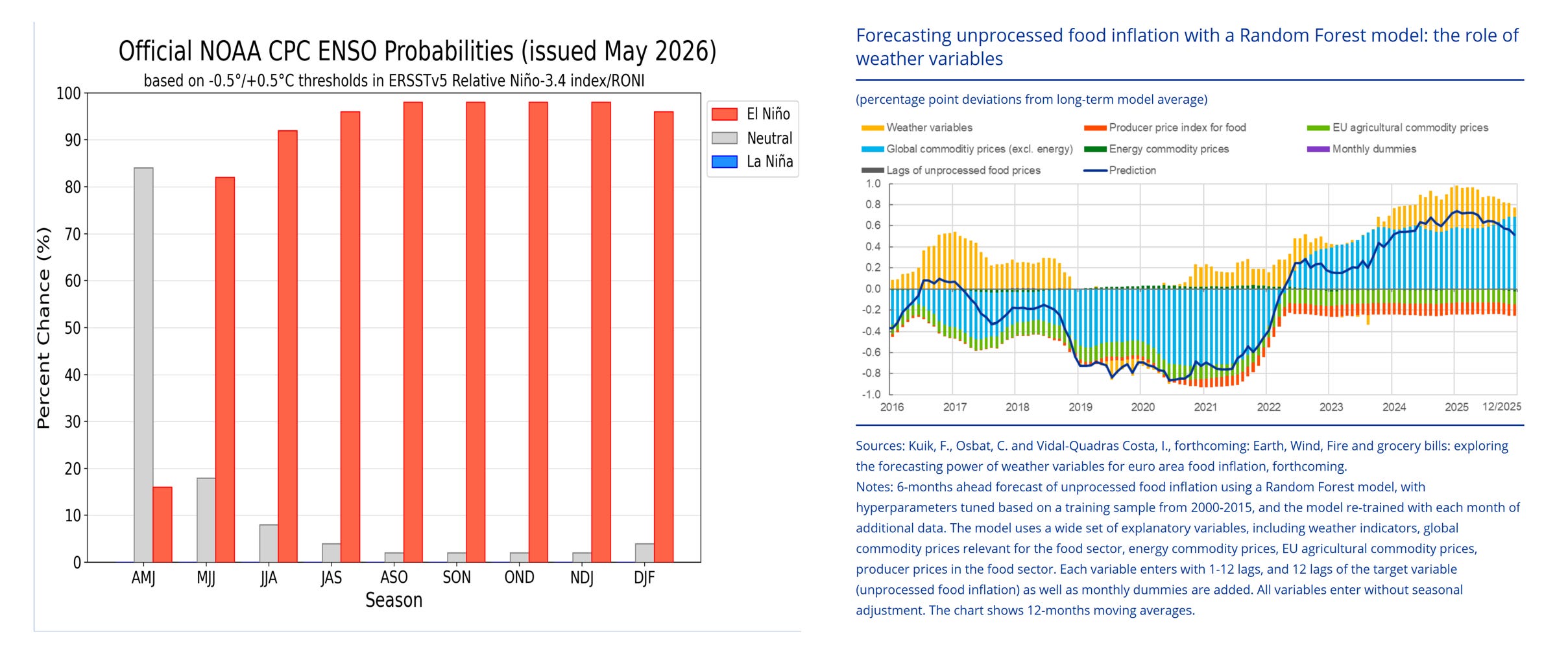

Latest predictions now put almost a 100% probability (almost, but not quite, but up from a probability of just over 60% a few weeks ago) to there being a El Niño this year (see first chart below), bringing with it the risk of runs of more extreme climate related events.

The next few weeks also brings with it more annual climate disclosures by central banks, including the WACI (weighted average carbon intensity) of their own reserve and QE portfolios, which in many cases are extensive.

Will the Bundesbank, for example, still own no Gilts (which score relatively well on the SECI), but lots of US treasuries (which score badly)?

Earlier this month saw the ECB - which in practice has more degrees of freedom to talk about all such things given its independence is enshrined in Treaty, as opposed to being granted only operational independence by Parliament - host a conference on the subject “Climate, Nature and Monetary Policy” which included keynote speeches by Christine Lagarde (see here) and Philip Lane (see here), which are definitely worth reading.

We were also interested in the piece the FT ran on Sarah Breeden, BoE Deputy Governor for Financial Stability a role, which includes monetary and financial stability risks stemming from climate change - note, Andrew Bailey steps down as Governor March 2028, sometime ahead of the next General Election, 15 August 2029, a key decision for whoever is UK PM and Chancellor will need to make.

And for those interested in the SECI please take a look at our more detailed research (which you can also sign up to on Substack), or our landing page with Solactive AG (for details see here).

Unlike UK PMs, climate change is not going away, and is a risk still not being priced into financial markets (something that the ECB continues to warn about). This includes government bond markets, as well as equities and credit, with clear implications for the loan books of banks and insurance corporations (which are already warning of the problems forecasting the costs of all such things, which they have to underwrite, or in some cases going forwards, not).

This research is for the use of named recipients only. If you are not the intended recipient, please notify us immediately; please do not copy or disclose its contents to any person or body as this will be unlawful. Information and opinions contained herein have been complied or arrived at from sources believed to be reliable, but Saltmarsh Economics Limited does not accept liability for any loss arising from the use hereof or make representation as to its accuracy or completeness. Any information to which no source has been attributed should be taken as an estimate by Saltmarsh Economics Limited. This document is not to be relied upon as such or used in substitution for the exercise of independent judgement.