The Art of the Deal

Views From the Marsh - David Owen

Two of my more abiding memories of the first few weeks after the UK’s EU referendum in 2016 was first, being led into the Court Room of the BoE (the symbolism of the room should not have been lost on anyone), for a speech by Mark Carney when he gave his own version of “whatever it takes” and second, an event organised by the Society of Professional Economists, where Professor Jim Rollo of Sussex University’s highly respected UK Trade Policy Observatory ran through the mechanics of actually negotiating trade deals.

Hours spent in rooms with no natural light, little food and stale coffee, all the while trying to navigate your way around complex rules of origin problems and a huge volume of documentation; the UK’s problem made worse by the loss of institutional knowledge about how to conduct all such things as, up until the UK’s departure from the EU, they had been handled by Brussels.

Such subtleties may currently not be on agenda of some of the US administration, but that is now the direction of travel for most of the large trading blocs involved, as well as countries like the UK. Slow everything down, and spend weeks and months re-negotiating and striking new trade deals, not just for goods, but for services (which can be even more complex); not quite sure what precisely, on a 5 year view, is the optimal strategy to employ, given things could look very different by then.

When it comes to trade, the US was never likely to be the Stackelberg leader, where everyone else will simply follow. This is much more complex and hence unpredictable. It should also be noted that traditionally when it came to the US, much of the trade negotiations have traditionally been conducted at the state, not federal level - another point that Jim Rollo made in 2016, making it more difficult to strike trade deals and obtain access to the wider US market.

As the FT’s Alan Beattie highlighted in his missive yesterday, the optimal strategy for the US’s trading partners may not to be to really engage too much with the US at the moment (partly because of how markets reacted), whilst exploring new and deeper trading relationships elsewhere, aware of the risks of trade diversion and dumping.

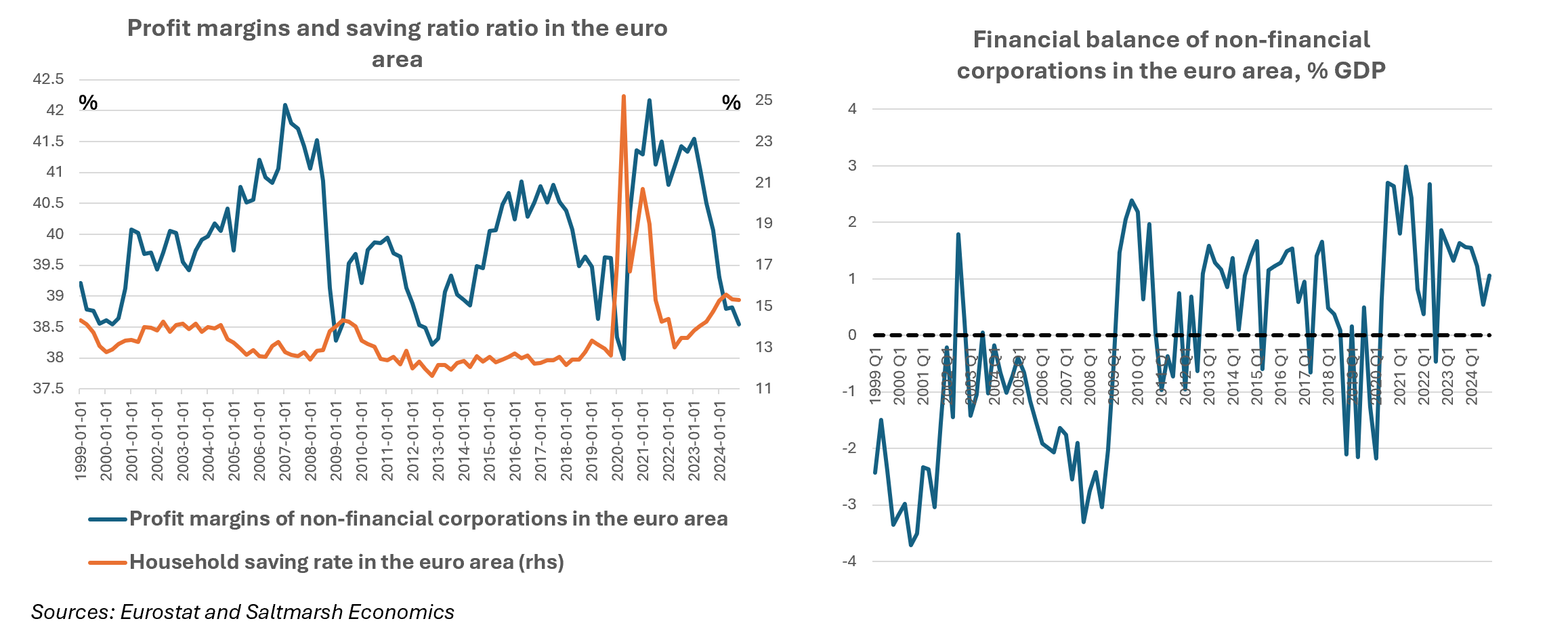

But, for the open euro area economy, it may now have to live with a stronger exchange rate, at the same time as corporate profit margins have come under pressure (see charts). Does that change the dynamics?

Keep reading with a 7-day free trial

Subscribe to Saltmarsh Economics to keep reading this post and get 7 days of free access to the full post archives.