Commercial Real Estate, Climate Risk and Stranded Assets

Watching the Tides - Marchel Alexandrovich

As we write about regularly, much of our research and consultancy work is focused on climate change and its impact on economic activity and policy. Two years ago, we launched our Saltmarsh Economics Climate Index (SECI), which scores and ranks countries based on climate risk factors. We now cover every economy included in the IMF database - 116 countries in total. The SECI combines a wide range of variables across two broad categories of macro data. The first category relates to the physical and transition risks associated with climate change. The second captures each economy’s capacity to absorb these risks and to withstand potential shocks. As an extension of this work, we have also developed an index that adjusts country weights in a benchmark sovereign bond portfolio. This index overweights economies less exposed to climate risks and underweights those more exposed. Please send us a message to schedule a meeting if you would like to discuss this index further.

Saltmarsh Climate Risk-Adjusted Sovereign Bond Index vs the FTSE WGBI DM sovereign bond benchmark

Source: Saltmarsh Economics

One important factor that has changed since we first launched our SECI scores is the weakening of the global political consensus on climate issues. The Trump administration has no interest in phasing out fossil fuels and cutting GHG emissions - that much is clear. But even in the UK, although there is no imminent prospect of the Labour government amending existing legislation and dropping the UK’s legally binding commitment to achieve net zero by 2050, climate change has suddenly become a politically divisive issue, with the Leader of the UK Opposition, Kemi Badenoch, recently describing herself as a “net zero sceptic” (someone who is not debating whether climate change exists, but does not think that the country should commit itself to the 2050 net zero target).

While in the political arena climate policy is still being debated, outside of politics, the markets are already actively pricing in the effects of climate change on asset values. In the US for instance, when investigating home insurance non-renewal rates, the Senate Budget Committee concluded late last year that, “across the United States, there is a clear correlation between non-renewal rate and climate risk. Additionally, areas with the highest climate risk also saw the largest increases in non-renewals from 2018 through 2023”. Insurance costs and non-renewal rates, in turn, will have an impact on property prices, mortgage valuations and credit availability.

Closer to home, the ECB recently published a study highlighting that higher temperature anomalies and more frequent natural disasters are already starting to be associated with lower sovereign credit ratings. At the moment, sovereign credit ratings, “seem to account for environmental considerations only partially.” However, the fact that the markets don’t fully incorporate climate related considerations means that, “there is a substantial likelihood of future repricing of assets exposed to these risks.”

In another recent piece of analysis, the ECB investigates the exposure of the euro area commercial real estate (CRE) market to climate related risks - both physical and transition. Buildings can obviously be damaged and destroyed during severe weather events. At the same time, they are responsible for around a third of EU’s energy related GHG emissions, and therefore older and less energy efficient properties are facing greater costs to help improve their environmental efficiency.

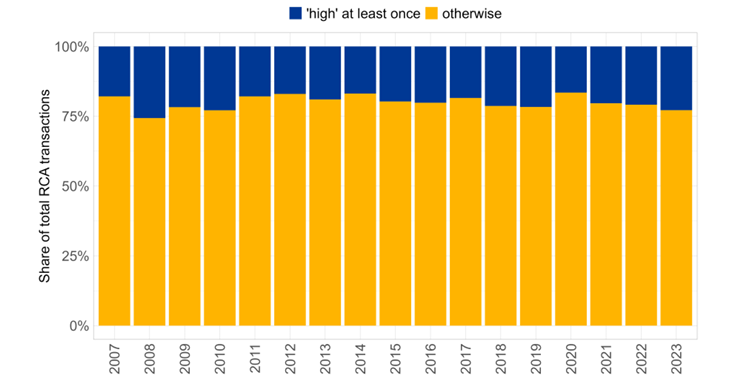

In terms of the study’s estimates of physical risk, it monitors the exposure of properties to earthquakes, floods, heat stress, sea level rises, water stress and wildfires, and then assigns risk scores (0=No risk; 1=Low risk; 2=Medium risk; 3=High risk; 4=Red Flag ) to each of the six factors. There are a couple of interesting observations that emerge from the data. The first, is that this is not a trivial issue: “a quarter of transacted buildings in each year have a high or very high risk score, (which) underlines again that euro area CRE markets have significant physical climate risk exposures.” The authors also observe that, “there is a clear divergence towards the end of the (time) series, with buildings exposed to physical risk largely excluded from the rapid price growth experienced in the market in the years prior to 2020.”

Share of annual office transactions with at least one High or Red Flag risk score

Source: ECB

Price per square foot of offices with at least one physical risk score equal to High or Red Flag and the rest of the market

Source: ECB

With regards to the estimates of transition risk, there is no reliable data on energy efficiency of the individual buildings that the authors could use. Instead, they focus on the age of the building and the time since the last renovation as a proxy of (future) higher transition costs. Similarly to what was seen on the physical risk side, the data “show a clear divergence between prices of buildings below and above the 5 year age cut-off in the final years of our sample.” Furthermore, “the premium for young buildings is significantly higher at the end of our sample than at the start, with a 18pps increase in premium over the 2007-2023 period” (see the second chart below).

Averages of transacted prices split across building age brackets

Source: ECB

Percentage point change in premia associated with an office being lass than five years old between 2007 and the year shown

Source: ECB

The authors note a modest decline in the premium assigned to newer buildings during the final years of the study. However, the more important finding arguably relates not to the price of the properties in the sample but to the liquidity conditions in the market. As they write: “market activity has shifted towards younger assets in the final years of our sample, even when we hold other factors equal and account for the supply of new buildings via construction activity.” Or, to put it more bluntly, “the ‘stranded asset’ problem arising from transition risk may already be beginning to take hold in euro area CRE markets.”

© 2025 Saltmarsh Economics Limited company Number: 13681146

Registered Address: Zeeta House 200 Upper Richmond Road, Putney, London, United Kingdom, SW15 2SH